"...the speed and magnitude of the Q1 downturn was unprecedented. It is also incongruous with, and an abrupt and brutal epitaph to the longest CRE market expansion on record."

Fundamentals in the small-cap CRE space market nose-dived during first quarter as the coronavirus pandemic triggered a massive economic retrenchment with wholesale employee layoffs, and company and store closures that now threaten the future of many Main Street businesses. The aftershocks of the disease outbreak starkly remind us of the binding and dynamic relationship between small business and small-cap CRE.

In the general CRE market at large, office and retail sectors suffered serious decreases in leasing volume. Yet the industrial sector, fueled in large part by Amazon’s signing of more than a dozen leases for about 10 million sq. ft., posted record leasing volume in Q1 according to CoStar. Frankly, the outbreak has only intensified the demand trend for large warehouse and distribution center facilities as retailers and direct-to-consumer businesses are swamped with online orders.

However, the pandemic's impact on small-cap CRE is extensive and perhaps more long lasting. Granted, we previously reported on a slow-moving contraction in small-cap CRE fundamentals caused by growing scarcity in both leasing availabilities and qualified employees for hire late in the CRE cycle. That said, the speed and magnitude of the Q1 downturn was unprecedented. It is also incongruous with, and an abrupt and brutal epitaph to the longest CRE market expansion on record.

×

![]()

Indeed, the sizable toll on small-cap leasing activity during Q1 was redolent of occupancy losses incurred during the Great Recession. Notable national statistics drawn from CoStar data solely involving small commercial properties under 50,000 sq. ft. include the following:

Space Demand Plummeted. While positive net absorption had already weakened considerably last year because of structural and capacity issues mentioned above, Q1 aggregate demand collapsed with occupancy losses totaling 13.8 million sq. ft. across office, industrial and retail sectors. This pullback was the first instance of combined, net negative absorption over 43 quarters dating to Q3 2009 when the market began its recovery from the Great Recession.

In particular, small-cap industrial demand plunged, accounting for nearly 10 million sq. ft. (70%) of the Q1 aggregate net negative absorption while also suffering occupancy losses for a third quarter in a row. We were in the throes of the previous recession when a similar set of contractions in industrial demand last occurred. Office demand also turned negative, at almost 3 million sq. ft., also for the first time since 2009, while the retail sector closed out Q1 with an occupancy loss of just over 900,000 sq. ft.

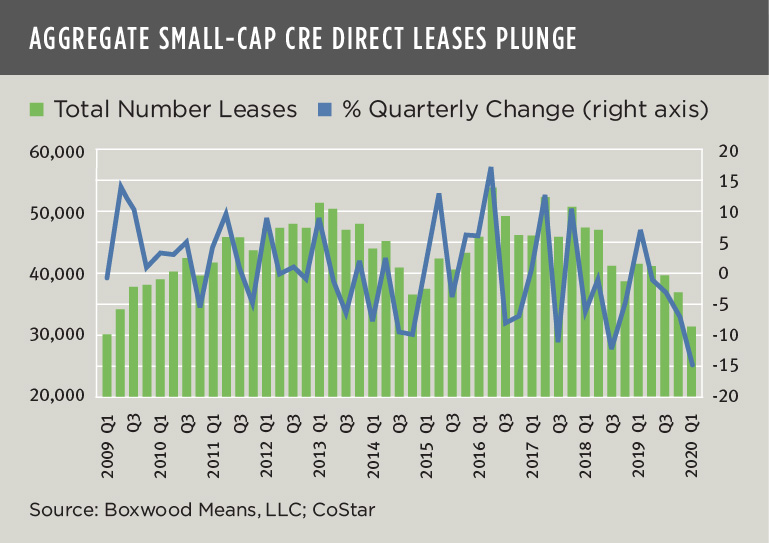

The nearby graph further illustrates the sharp reduction in demand as evidenced by the negative trend in direct signed leases across the three property types. Direct leases fell 14.8% sequentially to roughly 32,000 total contracts, the largest quarterly decline in at least 12 years.

Sublet Vacancies Jumped. Sublet activity had been increasing at a slow pace for several years running. But the Q1 volume of sublet space across the three property types jumped 11.5% to 31.1 million sq. ft., a level last reached in Q3 2010 when the market first found its footing. While industrial sublet space only accounted for about one-third of these total vacancies, this sector recorded the sole spike in sublet square footage among the three sectors by increasing a hefty 19% compared with Q4 of last year.

Overall vacancies edged up across the board. National average vacancy rates for industrial and office sectors rose 10 bps to 3.5% and 6.3%, respectively. However, retail vacancies increased 20 bps, to 4.3%, the highest level in 10 quarters. These national rates persist at levels considerably below historical norms.

Rent Growth Continued. Office asking rents posted an exceptional 9.3% YoY increase during Q1 to an average of $22.38 per sq. ft. following a huge 6.8% annual gain during the previous quarter. That these lofty figures contrasted sharply with the negative trend in office demand and signed lease contracts can be discounted by the lagging nature of asking rental rates and the indeterminate value of tenant concessions likely granted by landlords under softer space market conditions. Retail rents rose a healthy 3.8% YoY to an average of $19.61 per sq. ft.; but rent growth has generally traced a downward path for some two years. Lastly, industrial rents have come in for a soft landing. Annual rents averaging $9.98 per sq. ft. increased by 4.4% during Q1, far lower than the annual rate of 9.0% at this point last year and the lowest 12-month gain in 21 quarters dating to the end of 2014.

×

![]()

The demand and sublet statistics above portray a market poised for more turmoil. Unfortunately, the fallout will likely grow larger and broader by mid-year. After all, the Q1 statistics reflect changing market conditions for only two weeks’ time after Federal and State emergency preparedness and shelter in place mandates were implemented in mid-March.

This catastrophe reminds us that Main Street businesses, housed in a diverse array of light industrial, warehouse and manufacturing facilities, small office buildings and retail storefronts across the U.S., are the backbone of the small-cap CRE domain. What this interdependency has also unmasked, most vividly by the ubiquitous scenes of closed retail stores, is the fragile financial profile of many of these employers and business owners – especially their limited cash flow and credit – that calls into question their ability to withstand an economic disruption of this magnitude for a long period of time.

Let's hope and pray that the shutdown of our Main Street economy is short-lived.

Randy Fuchs

Randy Fuchs